Best Canadian Credit Cards

Sadly, the start of September meant the end of an era for my family. We said goodbye to our current credit card and went in search for the best Canadian credit card replacement.

For the past decade, we primarily used the Capital One Aspire travel rewards card — a card that offered 2 points for every dollar spent on everything, the ability to erase travel expenses (including taxes and fees) and a rewards program with no black-out dates, penalties or restrictions. Over the years, we funded trips to tropical locations, local retreats, many-miles of highway travel and even holiday trips to see our family in the U.S.

Sadly, these generous travel reward became yet another (albeit small) victim to the financial consequences of the COVID-19 pandemic. In early August, all cardholders were notified that the reward earnings would drop from 2x the points for every dollar spent to 1.5x the points for every dollar spent; that annual miles bonus that typically offered $100 to $150 in travel credits would be removed yet the annual fee of $120 to $150 (depending on when you applied and got your card) would remain the same.

Since earning 1.5 points for every dollar spent is now pretty standard for many reward or point cards — even those without an annual fee — it was time for our family to find a new credit card (or two). We were now on the hunt for the best Canadian credit card post-pandemic.

The problem, however, is that I am a serial comparison shopper. I rarely make a purchase without first doing quite a bit of research and, once complete, then comparison shopping for the best prices. And my analysis isn’t limited to the best price in online stores versus brick and mortar shops; my analysis examines pricing trends, best times of year to buy, as well as the new versus resale value.

While this might sound too laborious for some, I take a certain kind of pleasure in it. Chalk it up to that finance geek inside of me.

There are a number of exceptional ‘best of’ credit card rankings already in the marketplace (for a few good options, see below) and this is where I started my analysis. The problem is I don’t always know what I’m looking for when I first start researching. Ideally, I want to replicate what I had — 2 rewards for every dollar spent and rewards that could be applied against any travel expense, with no blackouts or restrictions, among other benefits. This rewards formulas had worked for us for almost a decade why not continue, right? But it wasn’t and, despite poking around for other cards over the years, I didn’t know how to rate the alternatives, quite yet.

Many credit card rankings will provide lists based on pre-selected criteria; some prioritize sign-up bonuses, others prioritize overall rewards, but I’m not a big fan of credit-card churning so I wanted to find the card that fit us and then use it for a long, long time.

I’m not against credit-card churning. I’ve done it before to juice reward points where a boost would help me achieve a target. When done smartly, credit-card churning can really help reward collectors — although there can be drawbacks, as well. I found the tasks of monitoring, tracking and maintaining each ‘temporary’ card (hold them for a year and then cancel so you are not charged the next year’s annual fee) was time-consuming; plus, I didn’t like the hard hits to my credit report. While these hits didn’t hurt me (I have a pretty good credit score), I imagine the obstacles some may face if these hard hits tell in a quarter (or year) when a loan or mortgage is up for renewal. Just one too many checks and your credit score could drop to a level that prevents you from getting the best possible rates on big loans. For a few extra reward points, the danger just isn’t worth it, for me.

As a result, I wanted a way to prioritize my specific needs without being forced into deciding what type of reward program I want. In the end, I’ll only go with an Air Miles linked card, a bank reward card, or any other reward program if the program actually delivered value.

To achieve my goal, I started a spreadsheet.

I know, not another spreadsheet, but truth be told I like the simple yet powerful way a spreadsheet allows me to list all the pertinent information while giving me the flexibility to shift the weighting of how I prioritized my needs or desires. So, if I really wanted a Mastercard, I could review all cards under the Mastercard brand, regardless of the reward program. A spreadsheet also enables me to take the time and energy spent into finding the best Canadian credit card in 2020 and use this work in the future.

To get access to the spreadsheet, click this link. Then copy the spreadsheet to your Google Drive and you can edit and use for your own personal use.

I wanted to identify personal credit cards, as I wasn’t looking for a card for my business, and I want to be able to sort based on type of card, size of annual fee, and overall reward terms. Finally, I tried to collect the most up-to-date promotions offered by each card. This is where data can quickly become outdated, so I didn’t want to weigh my decision solely on the promo offer. Instead, I wanted all my other needs met and find a card (and point in time) when it made sense to apply.

And, the best Canadian credit card in 2020 for my family is…

Once the spreadsheet was created, it was time to sort and decide. To do this, I had to create a list of criteria. While reward calculators are great to use, I find this tools pretty useless if I don’t first prioritize what I require out of my credit card — and my priority doesn’t start with amount or type of rewards I can expect.

For us, the criteria for our next credit card, or cards, included:

- a preference for Mastercard, as this would allow me to use it at Costco, where we spend quite a bit of money each year;

- a card that maximized the rewards for specific spending categories;

- a card that also enabled me to ignore or filter out categories that I didn’t care about, such as dining out;

- I didn’t want to be tied to specific stores or brands (I’m not about to drive around looking for a specific brand of gas station or only shop at one type of pharmacy)

- I would only pay an annual fee if the annual rewards could justify this fee;

- Finally, I wanted a card that made sense now (good promo points) and into the future.

For my family, the winning card was:

The Rogers Bank – World Elite Mastercard

The Rogers Bank – World Elite Mastercard

Why? We would get the same earn rate as our previous card but without the annual fee of $120. Plus, it allowed me to earn 1.5% cash back on all my purchases, unlike the Canadian Tire Triangle Mastercard series which denied the max reward earn rate for purchases made at Costco or Walmart, or capped max reward earnings after a certain amount, such as AMEX SimplyCash card.

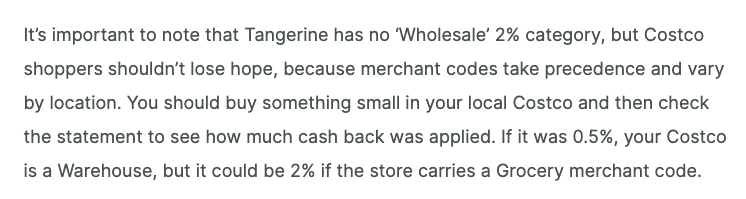

While I did toy around with the idea of getting a Tangerine Money-Back card or the Tangerine World Mastercard (and I may still), I didn’t like how each of the big box stores, such as Costco, Walmart and Superstore, could differ in how they were classified as a spending category. We do enough store jumping that I didn’t want to earn a paltry 0.5% just because a spending category code didn’t line up with my expectations. I’m not the only one concerned about this mislabeling.

While I did toy around with the idea of getting a Tangerine Money-Back card or the Tangerine World Mastercard (and I may still), I didn’t like how each of the big box stores, such as Costco, Walmart and Superstore, could differ in how they were classified as a spending category. We do enough store jumping that I didn’t want to earn a paltry 0.5% just because a spending category code didn’t line up with my expectations. I’m not the only one concerned about this mislabeling.

As Greedyrates points out:

Now, you may have more patience then me, but I’m not about to make a trip to Costco just to buy one small item to find out whether or not my credit card is giving me full rewards because the store is ‘classified’ correctly. I just don’t have that sort of time or patience.

Of course, if I only shopped at Walmart (or did most of my spending at this store), the Tangerine cards would win out. Again, as Greedyrates points out:

That doesn’t mean the Tangerine cash back cards — or any other card — isn’t a good bet. It just depends on your needs.

That said, we did actually end up applying and using a secondary credit card, the Canadian Tire Triangle World Elite Mastercard. Our rationale had nothing to do with the rewards — remember, I don’t like rewards tied to particular stores — but because this card offered free roadside assistance for all cardholders. Since we paid for BCAA anyway, it just made sense to get this roadside assistance coverage from a no-annual fee card and eliminate this fee from our family’s annual budget.

What other credit card holders say

Of course, finding the best credit card — and ranking these cards — is not an isolated endeavour.

Just about everyone has an opinion…and some of those opinions, I truly respect. Here’s a sample:

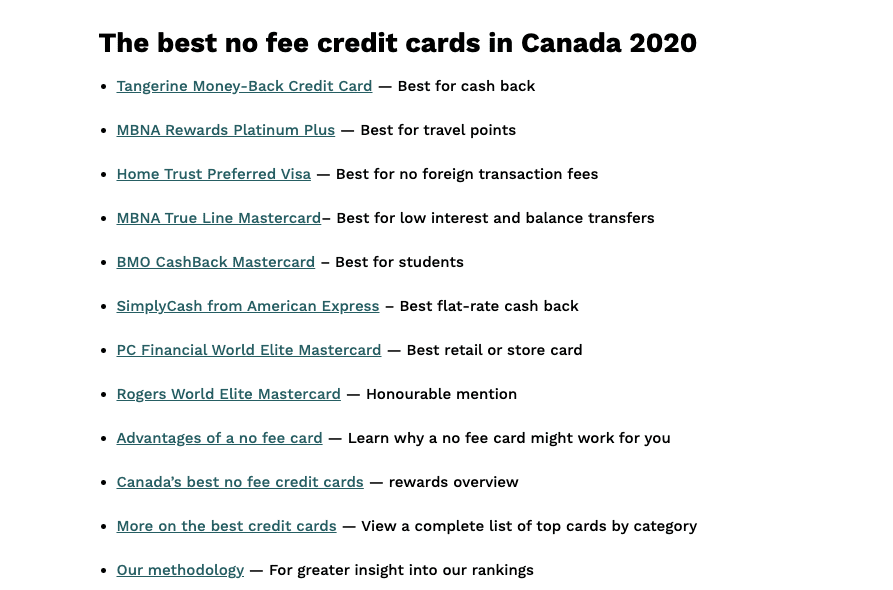

MoneySense offers an annual ranking that offers a list of best cards based on categories, such as best cash back cards, best low-interest cards, best travel rewards cards, best cards for those who spend on groceries or at gas stations among others. For instance, here is their list of best no-fee credit cards for 2020:

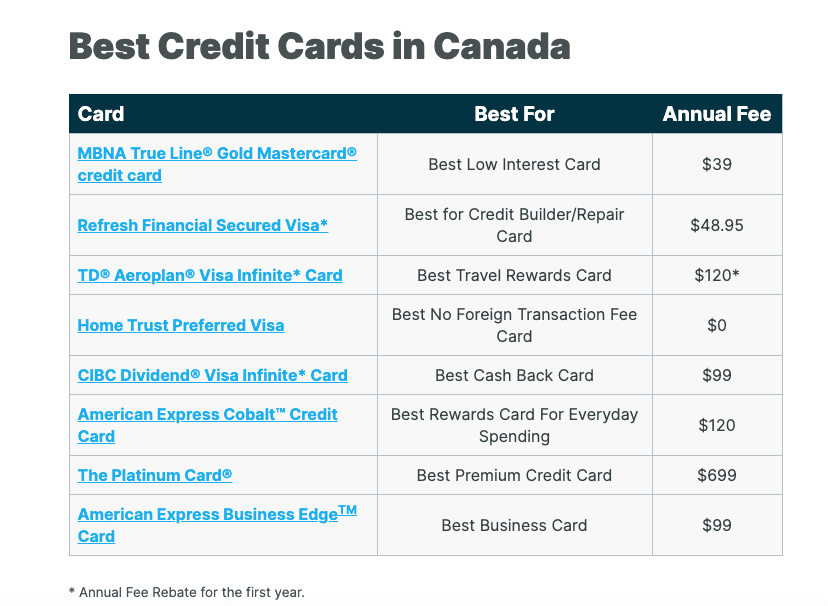

Ratehub also provides a best-of list:

As does Greedyrates:

Another option is to read or follow forums and community boards dedicated to tracking and discussing credit cards. For those interested in maximizing welcome or bonus points or those interested in learning how to church credit cards — the somewhat controversial practice of repeatedly applying for new charge accounts just to earn sign-up bonuses only to cancel the card before the next annual fee — check out the sub-Reddit forum:

General tips for choosing a credit card

When selecting a new credit card, first ask yourself: Why? Why do I need a new credit card at this point in time? The answer to this question will help you use the spreadsheet effectively and help guide you to the right card for you.

For instance, if you need a new card because you consistently carry a balance on your current credit card that has a high rate of interest, then you want to narrow down cards that offer low-interest (column XX). If you need a Mastercard (say, to maximize Costco purchases), then sort the sheet first based on the type of card (column XX) and then based on maximum rewards (column X).

To help you narrow down your options for getting a card, here is a quick definition of all the types of credit cards that are currently available on the market:

- Reward cards are credit cards that earn you points every time you use them to pay for items. These points are redeemable for various items, depending on the reward program. Most programs include redemption options for travel, airline tickets, cash back at stores (such as grocery stores or pharmacy retailers) as well as gift card purchases.

- Secured credit cards require that the cardholder deposit a certain percentage of the credit limit upfront into their bank accounts.

- Prepaid credit cards allow users with little, no or poor credit history to build their credit. These cards allow the user to get a card that allows you to deposit (or prepay) an amount on the card before using it to buy goods and services.

- Low-interest cards are credit cards that offer lower interest. These are best for people who carry a balance on their cards.

- Charge cards, also known as debit cards remove money from your bank account as soon as you pay for something using this card. You cannot carry forward a balance with a charge card (and, as a result, are not typically considered a credit card).

- Business credit cards focus on offering business-owners a variety of awards and services that meet entrepreneurial needs. To get a business card, you will typically need to show proof of a business such as a GST number, business number or business account.

Once you’ve narrowed down the type of card you need or want, it’s important to check the interest rate, known as the APR, or Annual Percentage Rate, especially if you plan to carry a balance on the card. For those that will carry a balance, try and pick cards with lower APRs. This will keep the interest you pay to a minimum, which helps you pay off outstanding balances faster.