Is Paying Off Your Mortgage Early Going to Ruin Your Finances?

Tempted to get rid of your mortgage early? Whether paying off your mortgage ahead of time is a good financial decision or something that will ruin your finances will depend on your individual situation.

If paying off your mortgage early is on your radar, comparing different options is essential in order to ensure you save money in the long run.

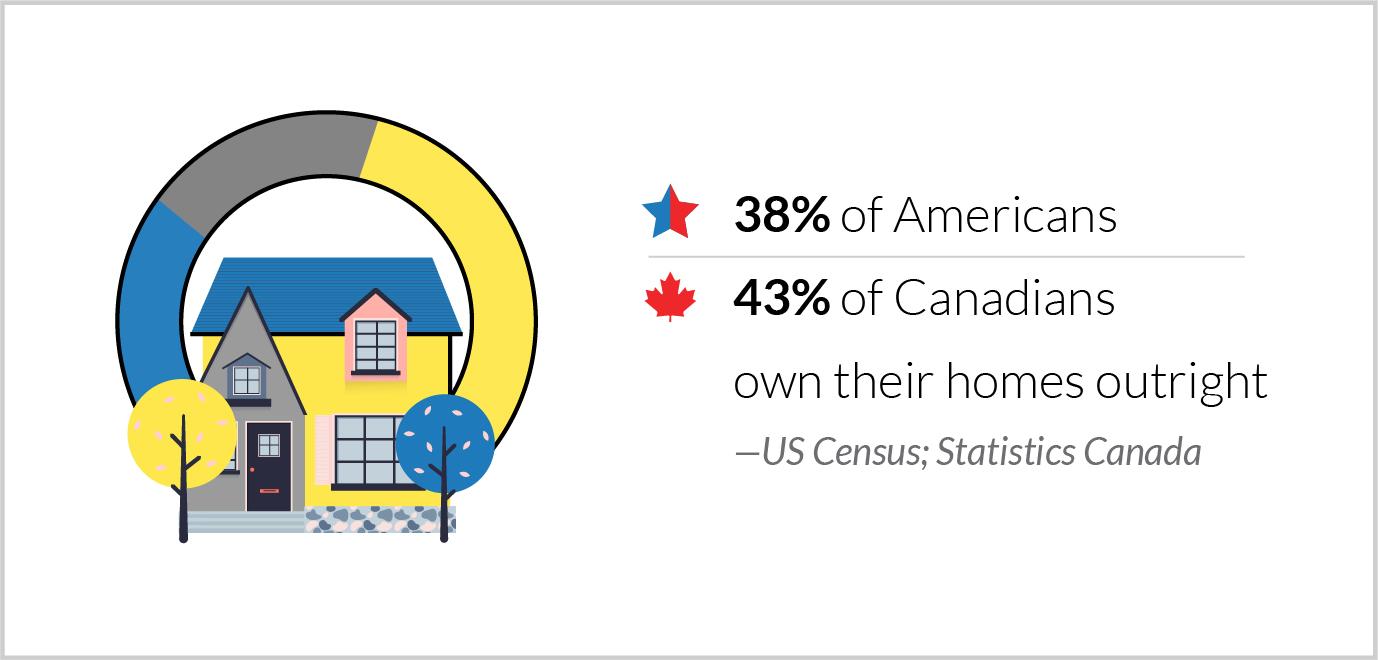

While owning your home outright and being able to put your monthly mortgage payments elsewhere might be tempting, it’s important to avoid putting your finances at risk by an uninformed decision.

This article will go through everything you need to know before you pay off your mortgage early.

Making Additional Mortgage Payments

Do you want to join the club and pay your mortgage sooner than you’ve originally planned?

You might be motivated to pay off your mortgage early by a vision of saving money on interest, getting the pressure of debt off your chest, and achieving the desired financial freedom.

There are a few different methods by which you can pay your mortgage before the scheduled timeline. The most common ones include:

1. Increasing Your Mortgage Payments

Increasing the amount you pay for your mortgage every month will help you to pay off the principal amount ahead of time. This can mean rounding up your payments from $780 to $800 or just adding extra 10 dollars on top of your monthly payments.

A small increase in monthly payments that you’ll hardly notice in your day-to-day life can make a significant difference in terms of your long-term finances.

Check the conditions in your mortgage contract and carefully consider your finances before you make the changes. Keep in mind that most of the time, you can’t reduce the amount back down after you’ve increased it.

This can be risky and if you don’t carefully plan this decision and don’t have substantial savings to back it up, it can leave you money-poor in the future.

2. Making a Lump-sum Payment

Making extra lump-sum payments in addition to your regular payments is a straightforward way of paying your mortgage ahead of time. You can simply schedule regular extra payments and complete 13 or 14 payments a year instead of the planned 12.

Many people choose to make a lump-sum payment with an unexpected income, such as bonuses or profits made from investments.

The lump sum you can make is usually between 10% and 20% of the original mortgage amount.

But because every mortgage contract is different, you should always check your conditions which will state specific times at which you are able to add lump-sum payments to your mortgage.

According to your contract, the lump-sum payments can be made:

- before the end of your term

- at the end of your term

- at certain times during your term

- on certain dates set out in your contract

Additionally, make sure that doing so won’t result in extra fees from your lender. This could cause that the fees are higher than the amount saved.

3. Choose an Accelerated Payments Option

With an accelerated payments option, you can choose biweekly payment instead of the usual monthly mortgage payment. This strategy can accumulate up to one extra monthly payment per year and allow you to pay off the mortgage loan faster.

An additional benefit of the accelerated payment option is saving money on interest rates.

4. Renegotiate Your Mortgage

Renegotiating your mortgage to pay it within a shorter period of time — known as a refinance with a shorter amortization period — only makes sense only if you can get a lower interest rate.

Keep in mind that refinancing often comes with refinancing fees.

In order to avoid losing money, make sure that the amount saved at the end of the loan period is higher than the refinancing fees.

You can refinance your mortgage and benefit from shorter loan terms, reducing your amortization period by several years.

To make sure you select an option that will benefit your long-term finances, compare the payments with a mortgage payoff calculator.

Advantages of Paying off Your Mortgage Early

1. Saving Money

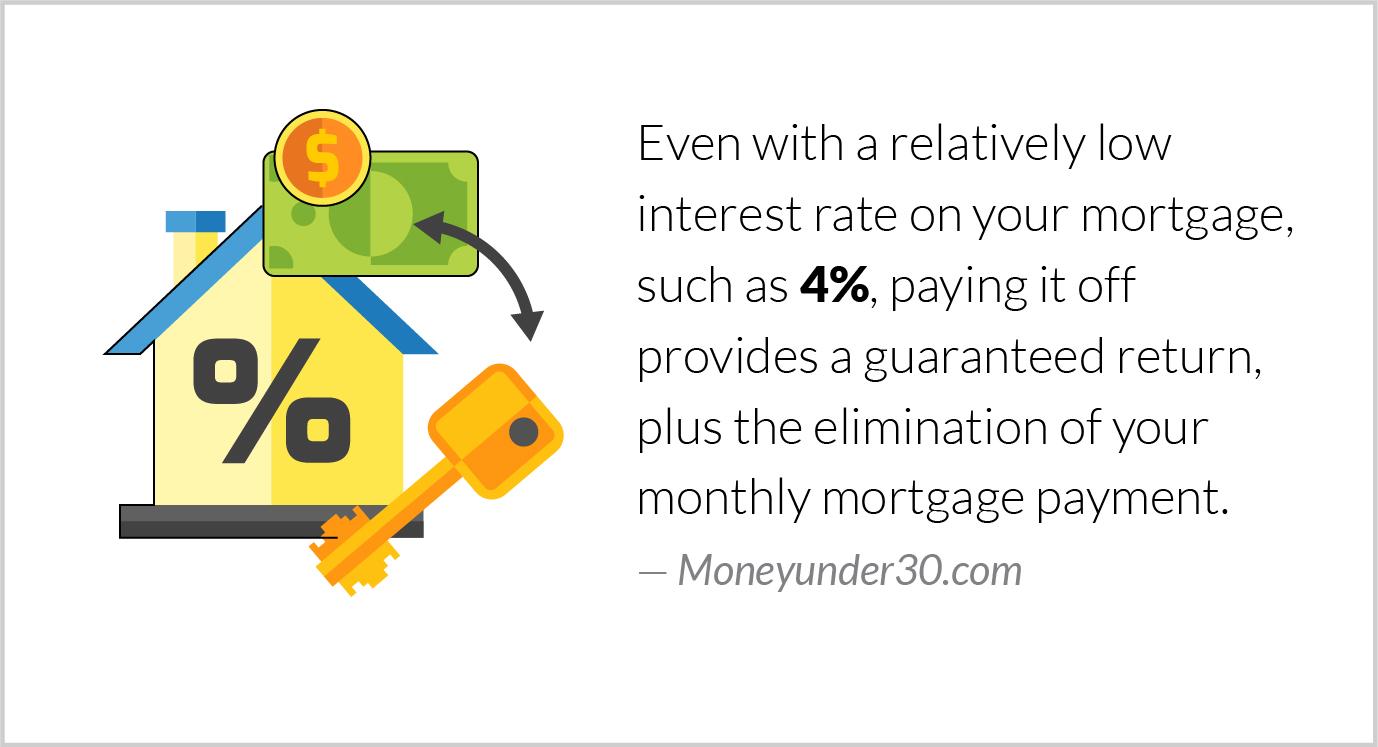

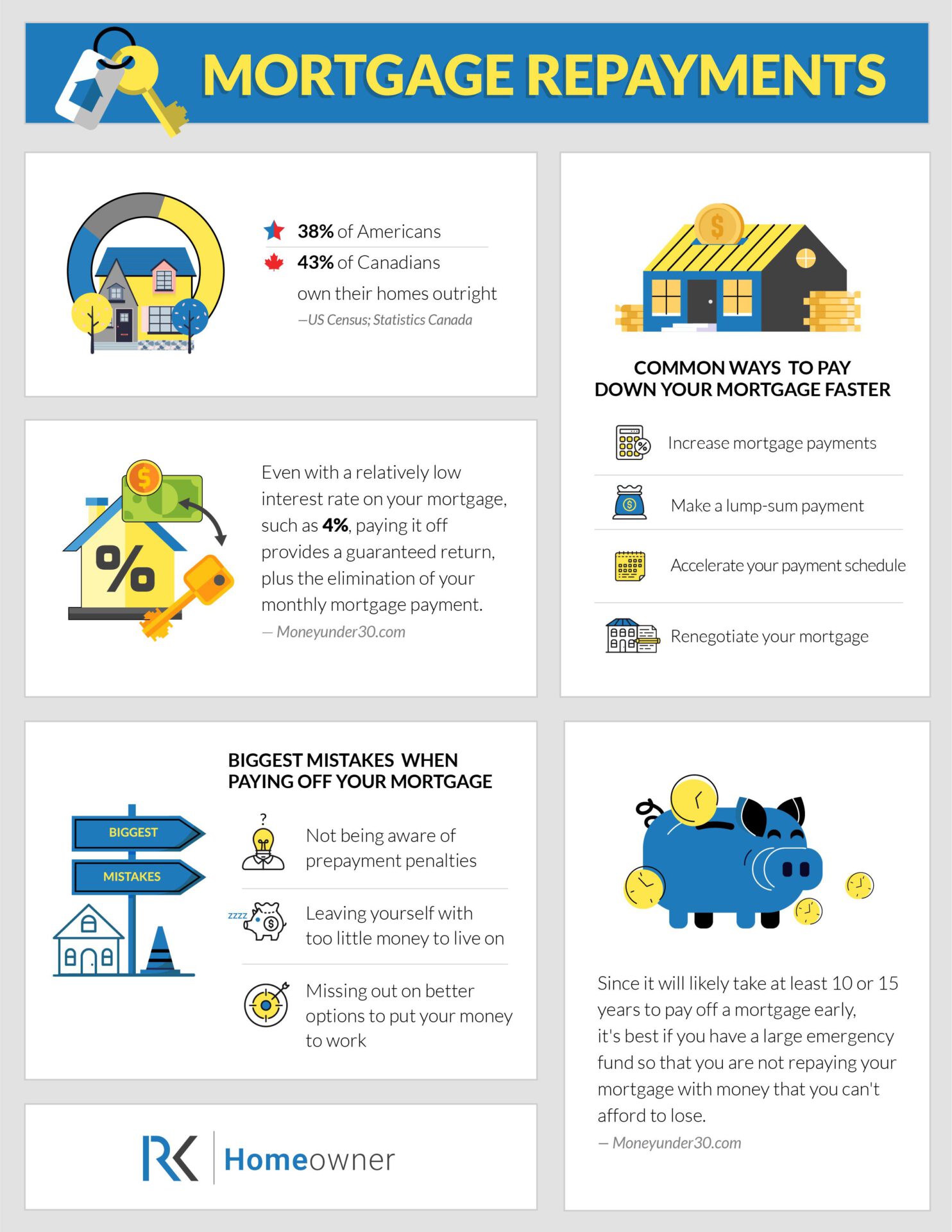

By paying your mortgage off early, you’re reducing your amortization. For example, by reducing the original 25-year amortization to 15 years, on the loan of $450,000 principal amount at 3% interest, you can save up to $80,000 on interest which you have to pay back to your mortgage company.

2. Getting Rid of the Debt

Many people opt to use their extra money for payments towards their mortgage in order to reduce the mortgage stress. This gives you the financial freedom to use your monthly mortgage payment money for other areas.

With no more debt, you can use the extra money to pursue your dreams. You can use the extra cash for traveling, retirement, or investment.

If you choose to invest, you can benefit further by gaining more income.

Are there any disadvantages to paying off your mortgage?

1. Avoiding the Risk

According to Forbes, rushing to pay off your mortgage early is one of the riskiest things you can do to your finances. If you increase your monthly payments, a decision that usually cannot be reversed, you lose the decision authority over your finances.

You hand it over to your bank instead.

And once you complete the extra payments towards the repayment of your mortgage, you can’t get the money back.

On the other hand, if you keep the money in your savings account, you can always access it and use the extra money where you need it the most.

And because you can never predict your future economic situation, putting an extra strain on your finances can be unnecessarily risky.

2. Low Interest

If you’ve secured a low interest rate for your mortgage, it might be financially smarter to take the extra payment and put it towards your credit card debt or pension plan.

If you’ve been paying the mortgage for an extended period of time and have an interest rate that is now a thing of the past, it’s a good idea to talk to your mortgage broker and look out for the lowest mortgage rates on the market.

3. Using the Money Elsewhere

Getting rid of the financial burden of your mortgage debt can sound like an attractive option. But the amount of money you save by paying your mortgage early can be much lower than the amount of money you can potentially make by investing it elsewhere.

Therefore, it can be smarter to invest your money into the stock or other assets. If you’re unsure about your options, seek investment advice from an experienced professional.

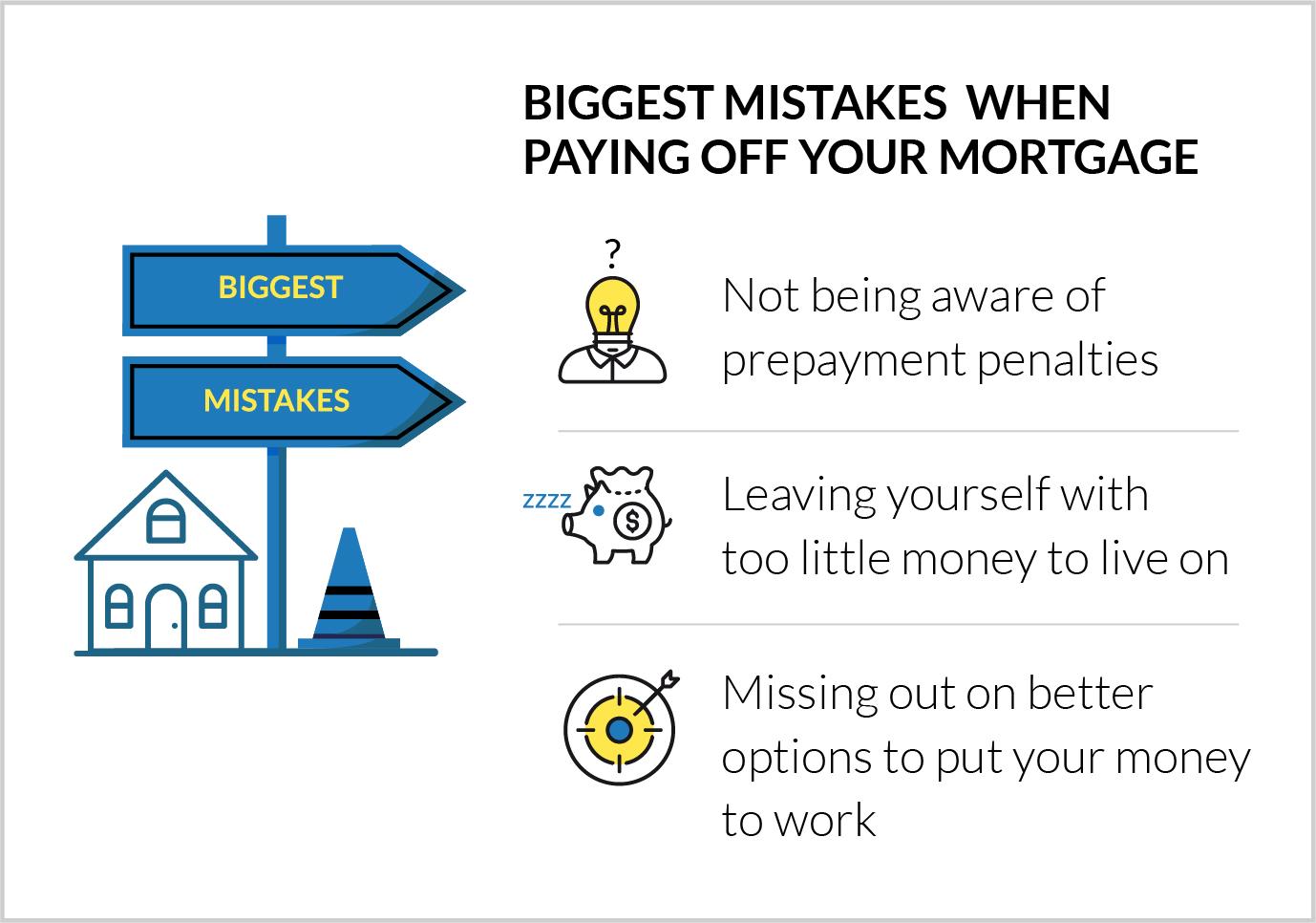

Most Common Mistakes People Make When Paying off the Mortgage Early

Considering paying off your mortgage early in order to save on interest? Avoid these most common mistakes people make when paying off their mortgage early.

1. Not Being Aware of the Prepayment Penalties

Prepayment penalties can be equal to a percentage of a mortgage loan amount or the equivalent of a certain number of monthly interest payments. These can quickly add up if you’re trying to pay off your 30-year mortgage early with extra payments.

If you don’t do make all the calculations and don’t talk to your financial advisor, you can actually end up losing money in the long run.

2. Leaving Yourself with Little Money to Live on

Rushing to pay off your mortgage with additional payments without having an emergency fund can leave you in a tight spot in the future.

Before you pour all your money into extra mortgage payments, focus on having six months of living expenses saved first. Once you establish better financial security, you can set up additional payments towards your mortgage.

3. Missing out on Better Options to Make Money

While it can be tempting to set up extra payments in order to reduce the amount of money you lose on the mortgage interest rate, investing the extra cash into stock can provide a higher rate of return.

Is Paying Your Mortgage off Early a Good Idea?

The decision of whether to pay off your mortgage early is the best option for you depends on how much extra money you can spare. While some general guidelines still apply, everyone’s financial situation is different and you should consider your circumstances before making the decision.

If you have extra cash and you’re considering shortening the loan term of your 15-Year mortgage, look at other options before you rush into it.

And if you’re struggling to make the decision on your own, consider talking to a financial advisor or mortgage broker to find the best strategy for you.