Impact of Tax on Our Earnings + How to Reduce Capital Gains Tax

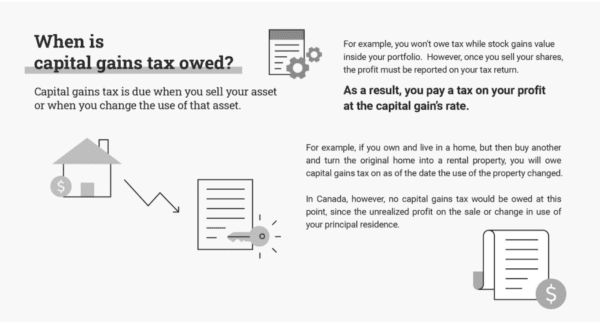

Capital gains tax is a tax that is levied on the profit earned from the sale of an asset, such as stocks, real estate, or other investments. The capital gains tax is calculated based on the difference between the purchase price of the asset and the price at which it is sold.

If the selling price of the asset is higher than the purchase price, the resulting gain is considered a capital gain and may be subject to tax. The capital gains tax rate varies depending on the type of asset sold and the length of time it was held.

In Canada, 50% of capital gains are included as part of your annual income and taxed at your marginal tax rate. However, there are some exceptions and deductions available, such as the principal residence exemption, which can shelter the entire profit on the sale of your home from capital gains tax. (And home does not mean a house, but can include a condo, townhouse, cottage, mobile home, and various other housing structures.)

How Capital Gains Tax is Calculated

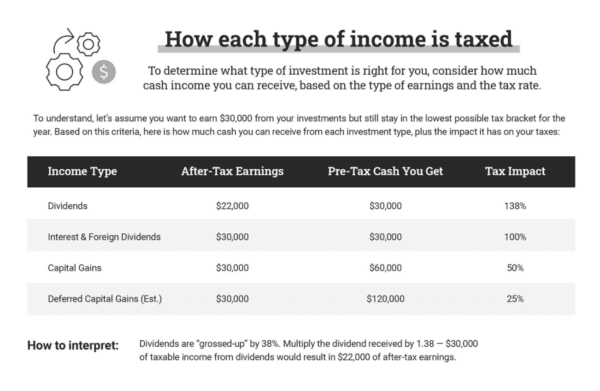

Advantage of the Capital Gains Tax

While most people seek ways to eliminate or reduce capital gains tax, it pays to remember that capital gains tax is far more generous than other forms of taxation.

How to Reduce or Eliminate Capital Gains Tax

Here are five last-minute tax planning tips and strategies for Canadians who sold property in 2022:

- Claim all eligible expenses: Make sure to keep all receipts and invoices related to the sale of the property, such as legal fees, real estate commissions, and renovation costs. If the property is not your principal residence — the property you use on a regular basis — then these expenses can be deducted from the sale price to reduce the capital gains tax you may owe on the profit made from the sale.

- Utilize the principal residence exemption: If the property was your principal residence for all or part of the time you owned it, you might be eligible for full or partial exemption from capital gains tax owed. Make sure to accurately calculate the years you lived in the property and the years you rented it out. Be sure you understand the +1 rule — which allows homeowners to claim two principal homes in one year, assuming that the reason for ownership in the same year was due to selling, moving and buying another residence.

- Consider the timing of the sale: If you have capital losses from other investments and plan on selling a secondary profit that has increased in value, consider selling the depreciated assets to take the tax loss. If the tax loss is large enough to reduce the gains to zero, capital losses can offset the current year’s capital gains and then carry forward to future years.

- Maximize your RRSP contributions: Contributing to your Registered Retirement Savings Plan (RRSP) can reduce your taxable income and help lower your tax bill. If you have any unused contribution room, consider contributing before the end of the tax year or before the RRSP deadline. (In 2023, the deadline was March 1, 2023.)

- Use a Tax-Free Savings Account (TFSA): If you have unused contribution room in your TFSA, consider contributing to the end of the tax year. Any gains earned within a TFSA are tax-free and while these gains won’t help offset the tax owed on assets that have appreciated in non-tax deferred accounts (or from the sale of a secondary property), the earnings can reduce the overall impact of the capital gains tax hit.

Keep in mind, there are no time restrictions imposed by the Canada Revenue Agency (CRA) on how long you must live in a home before claiming it as your principal residence.

Remember, expert advice is worth the cost. If your situation is complex or there are various factors involved, consult with a professional tax advisor or accountant for personalized advice on your specific tax situation.